| Date | Time | Currency | Headline | Actual | Expected | Previous | Impact on forex/equity markets |

|---|---|---|---|---|---|---|---|

| Tue, Jun 20 | 2:30am | AUD | Monetary Policy Meeting Minutes | N/A | |||

| Wed, Jun 21 | 7:00am | GBP | CPI y/y | 8.7% | 8.1% | GBP could weaken if inflation is higher than expected | |

| Wed, Jun 21 | 1:30pm | CAD | Core Retail Sales m/m | -0.3% | 0.1% | CAD could strengthen if retail sales are stronger than expected | |

| Wed, Jun 21 | 1:30pm | CAD | Retail Sales m/m | -1.4% | 0.4% | CAD could weaken if retail sales are weaker than expected | |

| Thu, Jun 22 | 8:30am | CHF | SNB Monetary Policy Assessment | N/A | |||

| Thu, Jun 22 | 8:30am | CHF | SNB Policy Rate | 1.50% | 1.50% | CHF could strengthen if the SNB raises interest rates more than expected | |

| Thu, Jun 22 | 9:00am | USD | FOMC Member Waller Speaks | N/A | |||

| Thu, Jun 22 | Tentative | CHF | SNB Press Conference | N/A | |||

| Thu, Jun 22 | 12:00pm | GBP | MPC Official Bank Rate Votes | 7-0-2 | 7-0-2 | GBP could strengthen if the BoE raises interest rates more than expected | |

| Thu, Jun 22 | 12:00pm | GBP | Monetary Policy Summary | N/A | |||

| Thu, Jun 22 | 12:00pm | GBP | Official Bank Rate | 4.50% | 4.50% | GBP could strengthen if the BoE raises interest rates more than expected | |

| Thu, Jun 22 | 1:30pm | USD | Unemployment Claims | 262K | 260K | USD could strengthen if unemployment claims are lower than expected | |

| Thu, Jun 22 | 3:00pm | USD | Fed Chair Powell Testifies | N/A | |||

| Thu, Jun 22 | 3:00pm | USD | Existing Home Sales | 4.28M | 4.22M | USD could strengthen if existing home sales are higher than expected |

Author Archives: Signal Setups

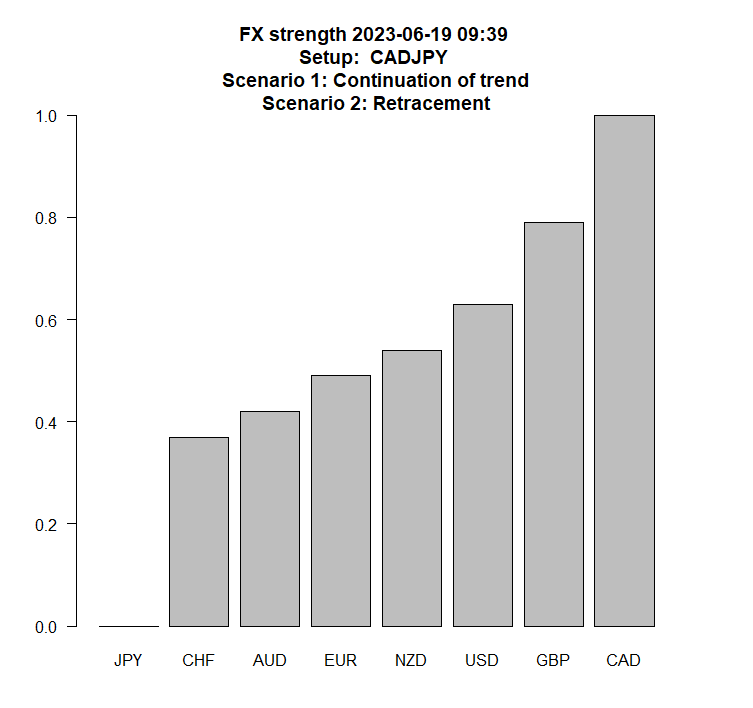

CADJPY

Week Ahead

- United States: The Federal Reserve is expected to continue its rate hike cycle, with Chair Powell testifying before Congress on Wednesday and Thursday. The housing market is also under close scrutiny, with data on building permits, mortgage applications, and existing home sales due out this week.

- Eurozone: The European Central Bank is also expected to raise rates, but the pace of tightening is likely to be more gradual than in the US. The ECB is also facing a number of other challenges, including the war in Ukraine and the risk of a recession.

- United Kingdom: The Bank of England is expected to raise rates for a fifth consecutive meeting. Inflation in the UK is at a 40-year high, and the BoE is under pressure to act to bring it under control.

- Other countries: Other central banks around the world are also expected to raise rates in an effort to combat inflation. The Reserve Bank of Australia, the Swiss National Bank, and the Bank of Canada are all expected to hike rates this week.

In addition to central bank policy, there are a number of other factors that could impact the markets this week. These include:

- US economic data: The release of key economic data, such as retail sales and industrial production, could provide insights into the health of the US economy.

- Geopolitical developments: The war in Ukraine and the ongoing tensions between the US and China could continue to weigh on investor sentiment.

- Corporate earnings: A number of major companies are scheduled to report earnings this week, which could provide investors with an update on corporate profits and outlooks.

Overall, the markets are likely to be volatile this week as investors assess the latest economic data and central bank policy decisions.

Roundup

- Japan released its monetary policy statement. The Bank of Japan (BOJ) kept its policy unchanged, as expected. The BOJ reiterated its commitment to maintaining its ultra-loose monetary policy stance.

- The US released its preliminary University of Michigan consumer sentiment index. The index rose to 63.9 in June, from 59.2 in May. The increase in the index was due to improved expectations for the future.

- The US Treasury Department released its currency report. The report showed that the US dollar’s share of global foreign exchange reserves fell to 58.6% in the first quarter of 2023, from 60.2% in the fourth quarter of 2022. The decline in the dollar’s share was due to increased demand for other currencies, such as the euro and the Japanese yen.

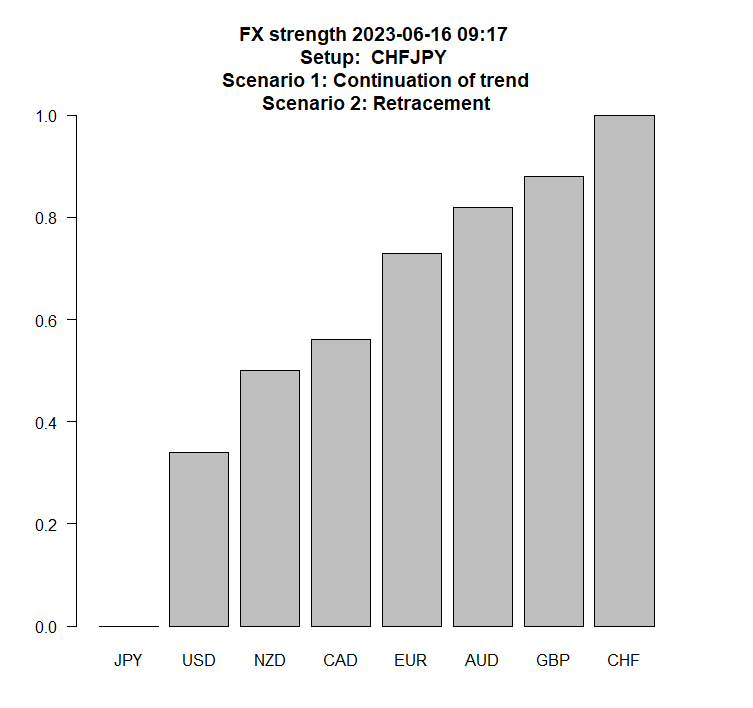

CHFJPY

Roundup

Roundup of the economic data released on June 15, 2024,

Australia:

- Employment Change: Came in at 75.9K, above the forecast of 18.6K and previous reading of -4.0K. Unemployment Rate remained unchanged at 3.6%.

- Market Impact: This is a positive sign for the Australian economy, as it suggests that the labor market is still strong. This could lead to higher stock prices and a stronger Australian dollar.

China:

- Industrial Production y/y: Came in at 3.5%, in line with the forecast and previous reading of 5.6%.

- Market Impact: This is a neutral result for the Chinese economy. It suggests that the economy is still growing, but at a slower pace than in previous months. This could lead to a slight decline in stock prices and a weaker Chinese yuan.

Eurozone:

- Main Refinancing Rate: Was kept unchanged at 4.00%, as expected. Monetary Policy Statement was also unchanged.

- Market Impact: This is a neutral result for the Eurozone economy. It suggests that the European Central Bank is not yet ready to raise interest rates, despite rising inflation. This could lead to a slight decline in stock prices and a weaker euro.

United States:

- Core Retail Sales m/m: Came in at 0.1%, the same as the forecast of 0.1% and previous reading of 0.4%.

- Empire State Manufacturing Index: Came in at 6.6, sharply higher than the forecast of -15.0 and previous reading of -31.8.

- Retail Sales m/m: Came in at 0.3%, above the forecast of -0.2% and previous reading of 0.4%.

- Unemployment Claims: Came in at 262K, higher than the forecast of 246K and previous reading of 262K.

- Market Impact: The mixed economic data released in the United States on June 15, 2024 is likely to have a neutral impact on the markets. The strong Empire State Manufacturing Index and Retail Sales m/m data are positive signs for the economy, but the higher than expected Unemployment Claims data is a negative sign. Overall, the data suggests that the US economy is growing at a moderate pace. This could lead to a slight decline in stock prices and a weaker US dollar.

Outlook

- Monetary Policy Statement (JPY): The BOJ is expected to keep its monetary policy unchanged at its meeting today. The central bank is likely to reiterate its commitment to maintaining a loose monetary policy in order to support economic growth. The meeting will start at 03:45 AM BST and is expected to finish at 05:00 AM BST.

- BOJ Press Conference (JPY): BOJ Governor Haruhiko Kuroda is expected to hold a press conference following the release of the monetary policy statement. Kuroda is likely to be asked about the central bank’s plans to address rising inflation. The press conference will start at 07:30 AM BST.

- Preliminary UoM Consumer Sentiment (USD): The University of Michigan Consumer Sentiment index is expected to show an increase from the previous month. The index is a closely watched measure of consumer confidence, and an increase could support the dollar. The index will be released at 03:00 PM BST.

Overall, the outlook for the USD and JPY is mixed today. The USD is expected to be supported, while the JPY is expected to weaken. However, the release of the preliminary UoM Consumer Sentiment index could provide some relief for the USD, while the BOJ’s monetary policy statement and press conference could provide some support for the JPY. Investors should monitor these events closely for any potential impact on currency markets.

Outlook

- Japan: A unchanged monetary policy from the BOJ is likely to be met with a muted reaction from markets. However, any changes to the BOJ’s assessment of the economy or inflation could move markets.

- United States: A strong reading on the University of Michigan consumer sentiment index could boost investor sentiment and support stock prices. However, a weak reading could weigh on investor sentiment and pressure stock prices.

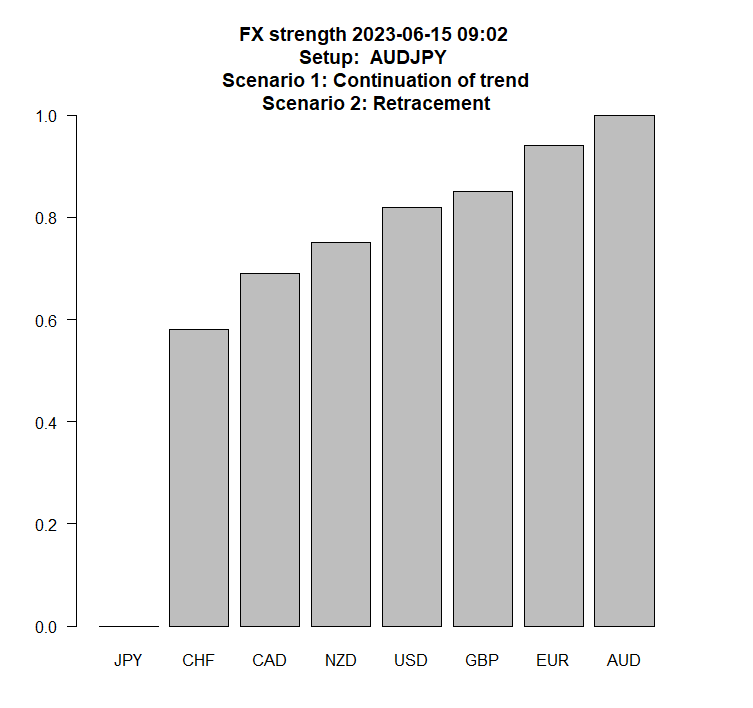

AUDJPY

Key Economic News for Thursday, June 15, 2023 (UK time).

Australia will release its employment change and unemployment rate data at 2:30am . A stronger-than-expected employment report could boost the Australian dollar.

China will release its industrial production data at 3:00am . A weaker-than-expected industrial production report could weigh on the Chinese yuan.

The European Central Bank (ECB) will hold its monetary policy meeting at 1:15pm . EUR/USD could rise if the ECB raises interest rates.

The United States will release its core retail sales, Empire State Manufacturing Index, retail sales, and unemployment claims data at 1:30pm . A weaker-than-expected retail sales report could weigh on the US dollar. A stronger-than-expected Empire State Manufacturing Index could boost the US dollar.

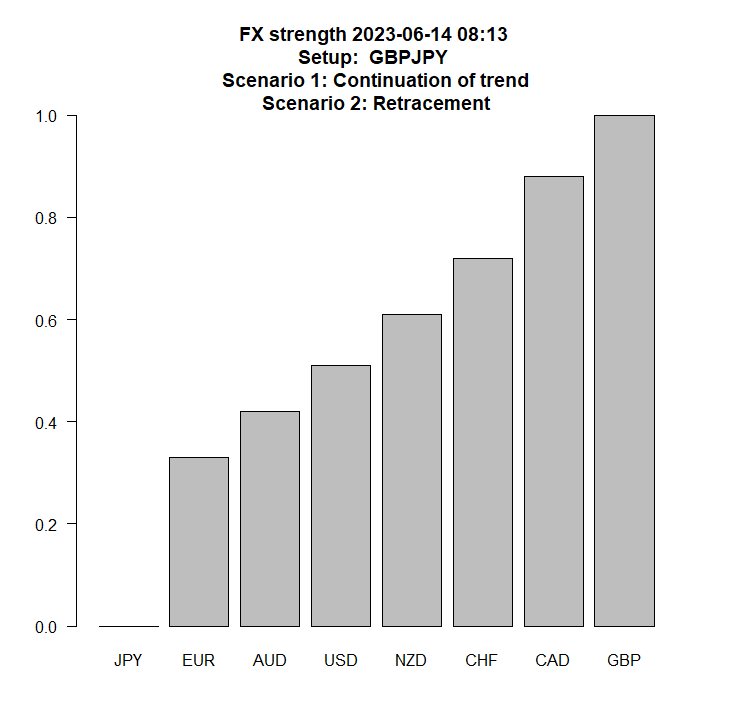

Setup: GBPJPY